It will take more than just studying for your kids to make it across the college finish line—namely, it will also take buckets and buckets of cash. More specifically, one year at an in-state public college costs about $26,000, including room, board, and books. The average cost at private colleges is more than twice that—about $53,000 per year.

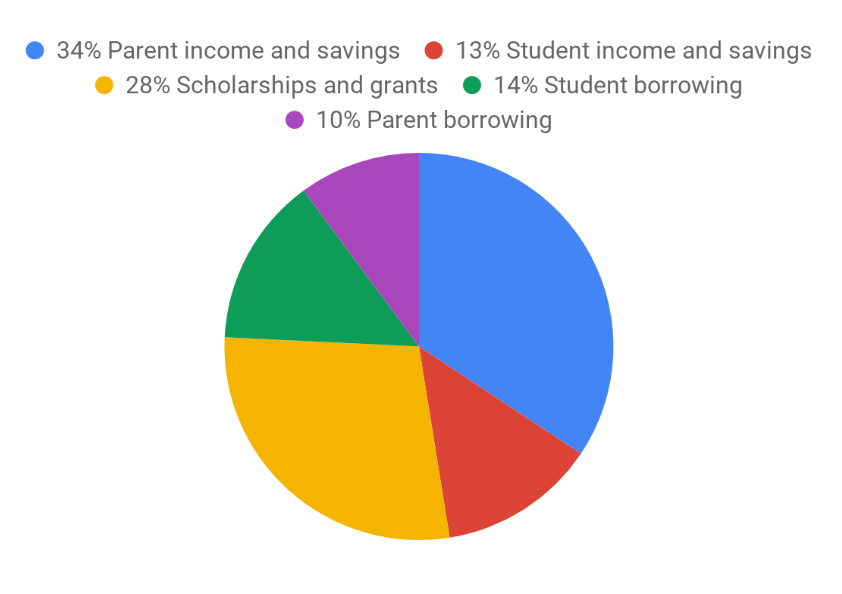

How a Typical Family Pays for College

Although those numbers are certainly eye popping, most families don’t pay sticker-price figures out of pocket (and they certainly don’t bankroll the whole tab with debt).

Instead, the average student’s funding sources look like this:

Source of Financing a College Education

- Income and savings—chances are both you and your child will need to contribute pretty heavily.

- Scholarships and grants—aka free money! These may be based on financial need, academic merit, or other factors.

- Work-study jobs—one perk is that unlike other jobs income from these jobs doesn’t count against your family in financial aid calculations.

- Federal loans—money your child, or you, borrows from the government, usually at a low interest rate. These loans come with certain protections if your kid faces financial hardship after graduating.

- Private loans—money borrowed from a private entity, usually at a higher rate and with fewer protections. If your child takes out a private loan, you’ll typically need to cosign.

- Tax credits—you may be able to claim a tax credit for some amount of what your family spends on tuition and other expenses.

- Military service—if your kid serves in the military for a certain length of time before attending college, he or she may qualify for education benefits.

Tips for Paying for College

There’s no magic wand that can transform paying for college into an easy feat. But here are some pointers to keep in mind:

- Watch your deadlines.

- You won’t get any aid if your family doesn’t apply, so be vigilant about learning all deadlines that may affect you. The Free Application for Federal Student Aid (FAFSA) typically opens on October 1, and experts say there’s no reason not to apply early.

- Leave no stone unturned in the search for free money.

- Your child’s college financial aid office can help with finding opportunities, but your family should also do your own research to find private scholarships.

- Avoid big checks written out to your child.

- Assets owned directly by your child are typically assessed more heavily in financial aid calculations than assets that you own.

- If a well-meaning friend or family member wants to help, instead of writing a large check to your child, let them pick up the tab for books for the year or find another workaround.

- Don’t sacrifice retirement.

- Financial experts strongly recommend that you avoid dipping into your own retirement savings to finance college. After all, there are no loans for retirement.

Some Fun Facts about Paying for College

There are actual scholarships available for vegetarians, for being left-handed, for being tall (or short), and for people with the last name “Zolp.”

Prices at private colleges have been rising at more than twice the rate of inflation in recent years.

Key Takeaways

College is incredibly expensive, though most families get some relief from grants and scholarships.

In addition to that “free money,” a typical family uses a combination of savings, income, and loans to afford college.

To help ease the burden, make sure you stay on top of aid deadlines, conduct a comprehensive search for grants and scholarships, and avoid dipping into your retirement savings when it comes time to pay.

You May Also Enjoy:

What You Need to Know about the FAFSA and CSS Profile

Seven Most Frequently Asked Questions About Paying for College